How VCs Are Approaching Valuations in 2024

I recently chatted Lisa Calhoun of Valor Ventures and asked her how their firm was handling the significant reset of company valuations between 2021 and now.

She had a great response that I think is helpful to everyone in Startupland, especially founders who are raising right now.

She said, “Show founders the VC math.”

Here’s what she meant — in 2 formats — since some founders only have 2 minutes and others love the deets!

TL;DR

Investors are looking for a 10x return based on current exits in your market.

Work backwards to figure out a current valuation with those market comps.

If that was gibberish to you, no problem! Here is the full explanation with math, valuation charts, action item, and OF COURSE, the O’Daily calling card, a numbered list!

1. Pursue a 10x return.

It’s venture capital industry standard to invest in companies that have the potential to 10x your initial investment.

If it’s an early stage — like seed or pre-seed — they’re likely looking for 10-20x since it’s higher risk.

Why?

Because VCs have bosses!

Their bosses are entities like hospitals, endowments, and pension funds, who are counting on the money invested to increase in value for their constituents.

So how do you get a 10x return?

You invest $1M into a startup in the hopes that in 5-10 years, your investment is worth $10M.

Why 10x?

Many companies will end up at 1x or 0x.

A few companies will be 3-5x.

If things go well, 1 or 2 companies will be big and “return the whole fund.”

So you need to have a path to 10x in every investment to cover the ones that inevitably won’t work out.

If you start out with an upper limit of only 5x, you’re screwed!

If you’re pre-Series A, it’s even riskier so you need to shoot for 20x potential returns.

ICYMI — same math applies for founders which is why I talk about picking a big market here, here, here, here, and here!!!

2. Study exits in your industry.

What companies in your industry recently had exits?

Usually this means being acquired, sometimes it’s going public.

What were the economics of those exits?

In other words, how much was the company worth compared to its revenue (or EBITDA for later stages)? 5x revenue? 10x revenue? 3x revenue?

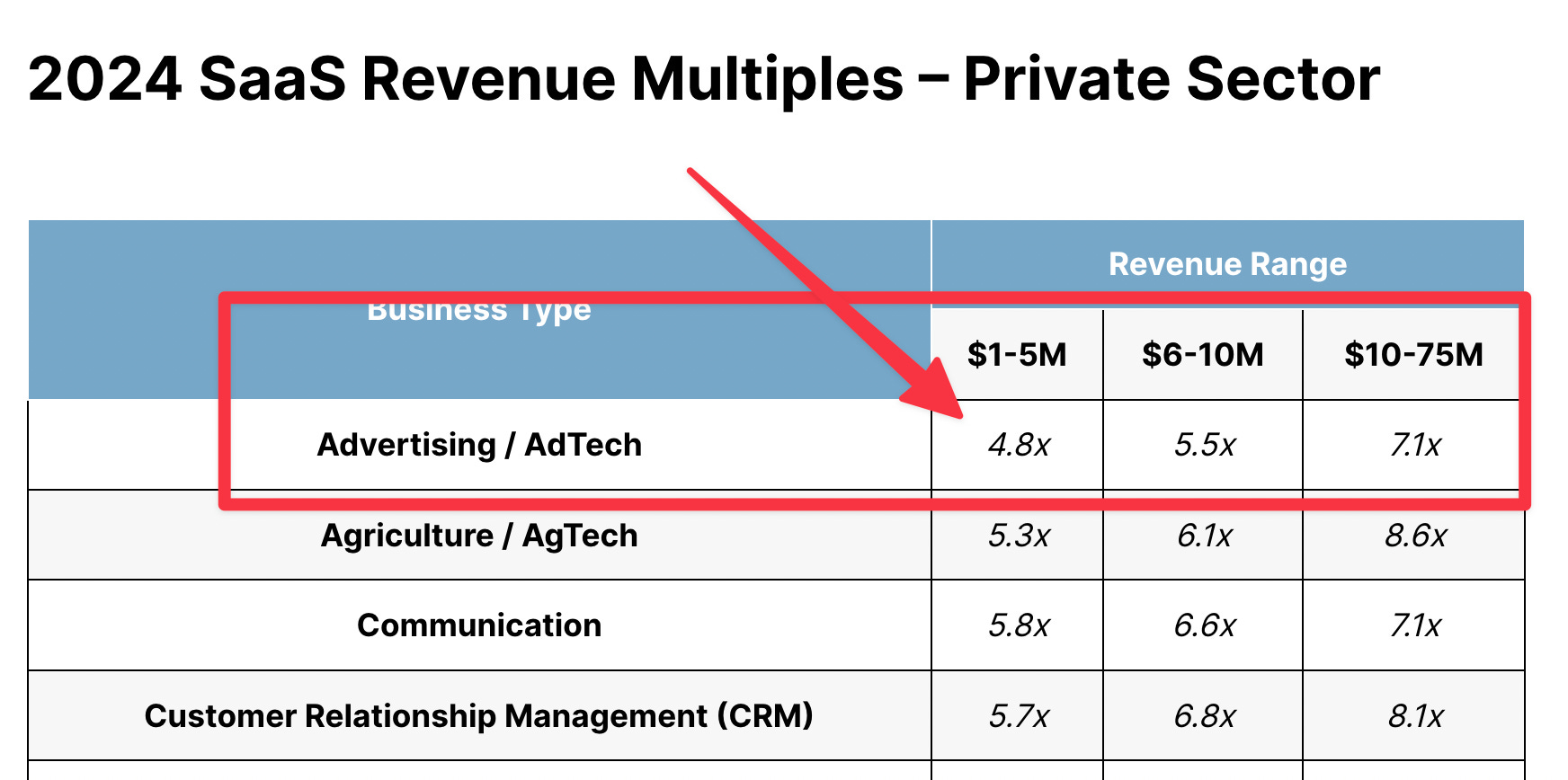

Here is a chart of 2023 SaaS trends for reference and another great chart that showcases the range and factors of valuations across industries. Business model, sector, growth rate, recurring vs non-recurring revenue, future potential, and a myriad of other things can impact valuations.

Helpful to note: public market valuations directly impact early stage private companies. They set the benchmark and everyone starts doing math based on those “end game” numbers.

So what does this mean for your company right now?

Here’s a simple example:

Based on the 2023 SaaS trends data, if you have a B2B SaaS company in adtech, when (not “if”!) you get to $10M ARR, you’ll get a 7x multiple or $70M valuation.

3. Work backwards to today.

What is a reasonable best-case-scenario for your company?

What is the right valuation now that enables an investor to get a 10x return?

This means that for your hypothetical $70M exit, an investor would need to invest today at a $7M valuation.

I’ve built out an elaborate formula for this:

$7M * 10x = $70M

You’re welcome. 🧠🥳💰

Of course, this assumes that you can get to $10M ARR without more investment.

If you take more investment, there’s more dilution, so the valuation would need to be even lower today to get a 10x return later.

More math:

$7M * 10x = $70MYou raise another round and everyone is diluted 20%…The company has to do 20% better in the exit -OR- starting valuation is 20% less

$7M * 80% (aka 20% less) = $5.6M

So $5.6M for your current valuation with one round of dilution to get 10x return

Let’s add a second round of dilution just in case things don’t go exactly as planned:

$5.6M * 80% = $4.5M

Not surprisingly, if you’re around $1M in revenue, this $4.5M valuation is pretty close to the 4.8x multiple from this chart:

It’s obviously not an exact science but this is back-of-the-napkin math to show you how investors are thinking about valuations right now.

Want to do your own math?

Here’s a simple dilution calculator from Atlanta Ventures to map out more investment rounds, include an employee option pool, or test different scenarios!

4. Remember your fundraise amount signals valuation.

If you’re relatively new to the world of VC, here’s a reminder about the most important unspoken math:

VCs assume that you’re offering 15-25% of your company

Whatever your fundraise ask is ~20% of your company’s value

Put another way: Fundraise $$ Ask * 5 = Your Implied Valuation

Yes, there are exceptions and negotiations but this is a helpful ballpark.

When you ask for a high dollar, it implies a high valuation, not high dilution (e.g. willingness to offer 50% of your company).

5. Compare this valuation to yours.

The reckoning!

Take the VC math and compare it to your current fundraise and/or last round valuation.

Close? Far? Way far?

The market has changed drastically so 99% of companies that raised in 2021 or 2020 will not love the math they see.

This isn’t a reflection of you or your company!

You may have executed perfectly, crushed your forecast, got amazing customer feedback, built the best product, and still not see a number you like.

Everyone in Startupland understands the shift.

Even top founders (and investors!) can’t control things like timing, luck, and the stock market.

6. Decide what (if any) actions to take.

I share all this to provide info and awareness.

This is the math investors are doing.

You chose what action, if any, to take.

Oh, and by the way — there are still companies raising money on better-than-industry valuations.

I know 2 companies in Atlanta this year that raised money on a 2-3x valuation of their previous round.

So there may be no action to take!

Maybe you double down on your current strategy. Maybe you tweak expectations. Maybe this is a wakeup call for a big change.

There are many paths, all with tradeoffs. Such is the nature of startups!

As you think it through, here are some questions that may help.

Valuation & Action Plan Questions

If I raise a round at a “VC math” valuation, what does that look like for me and the team? What will the cap table look like afterward?

What kind of exit makes it “worth it” at a new valuation? How many years or dollars until we get there?

Can I make a compelling case for better-than-industry potential and returns?

How much money do we need to get to the next milestone (raise, breakeven point, traction)? Can we get there with less money? What does that look like?

Are there any investors that passed because of valuation? Do different economics change the conversation?

What have my current investors advised? (While I think it’s commendable to protect the interests of current investors, they should understand the market. They can put in money themselves if they are pushing for a certain valuation.)

What other tips do you have around fundraising or valuation with the market shifts?

Any terms or concepts in this post that I should explain further? There is a lot of industry jargon!